published: 01/19/2016

Resolution No. 43 is aimed at uniformity of judicial practice. I would like to draw your attention to one of the clarifications contained in this document that is of significant importance.

In particular, paragraph 2 of this Resolution clarifies issues related to the beginning of the limitation period. By virtue of paragraph 1 of Art. 200 of the Civil Code of the Russian Federation, unless otherwise established by law, the limitation period begins from the day when the person learned or should have learned about the violation of his right and who is the proper defendant in the claim for the protection of this right.

The Supreme Court of the Russian Federation indicates that the limitation period also applies to legal representatives, including the guardianship and trusteeship authority. In other words, the period begins from the day when the legal representative learned or should have known about the violated right.

You may be interested in: Subscription legal services.

The provisions provided for in paragraph. 5 tbsp. 208 of the Civil Code of the Russian Federation, do not apply to claims that are not negative

The explanations contained in paragraph 7 of Resolution No. 43 are also important, since in some cases the content of paragraph. 5 tbsp. 208 of the Civil Code of the Russian Federation caused difficulties for the courts. The Plenum indicates that the provisions provided for in paragraph. 5 tbsp. 208 of the Civil Code of the Russian Federation do not apply to claims that are not negatory (for example, to claims for the recovery of property from someone else’s illegal possession).

It follows from this that the general limitation period of 3 years applies to claims for the recovery of property from someone else’s illegal possession. In other words, Article 208 of the Civil Code of the Russian Federation is not applicable to a claim of a vindication nature, but if we are talking about negative claims, then the limitation period by virtue of paragraph. 5 tbsp. 208 of the Civil Code of the Russian Federation does not apply to them.

The position of the Supreme Court of the Russian Federation, set out in paragraph 10 of Resolution No. 43, has significant law enforcement significance. The Plenum indicates that the statement on the application of the statute of limitations made by one of the co-defendants does not apply to other co-defendants.

At the same time, it is clarified that the court has the right to refuse to satisfy the claim if there is an application for the application of the limitation period from only one of the co-defendants, provided that by virtue of law or contract or based on the nature of the disputed legal relationship, the plaintiff’s demands cannot be satisfied at the expense of other co-defendants (for example , in case of filing a claim for the recovery of an indivisible thing that is jointly owned by several persons).

This approach will eliminate legal uncertainty on issues where the application of a statute of limitations contradicts the nature of the obligation arising from claims against several persons.

In paragraph 12 of Resolution No. 43, it is concluded that the burden of proving the presence of circumstances indicating a break, suspension of the limitation period rests with the person who filed the claim.

You may be interested in: Pre-trial dispute resolution.

Limitation period - duration, interruption

Before going to court, it is necessary to determine whether the statute of limitations has expired, since if it is missed, there is a high probability of denial of the claim. In accordance with Art. 199 of the Civil Code of the Russian Federation, if the deadline is missed, the court is obliged to accept the claim. BUT, if a party to the case (the defendant) declares that the limitation period has been missed, then in this case the court will reject the claim in whole or in part due to the missed limitation period. That is, even if the claim is subject to satisfaction and there are all grounds for this, the plaintiff’s right is actually violated, the satisfaction of the claims will still be refused.

The concept of a statute of limitations

The limitation period is the period for protecting the right under the claim of a person whose right has been violated. That is, a person whose right has been violated can, within a period specified in law, go to court with a demand from the obligated person to restore his violated right.

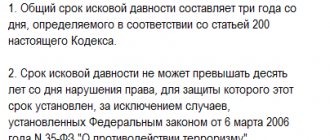

The general limitation period is 3 years.

By general term it is meant that it is subject to application in all cases where special terms are not established by law.

Special limitation periods may be longer than the general period or shorter, but they are necessarily established by law. For example, the shortened statute of limitations under a property insurance contract is 2 years, and the shortened statute of limitations is established for claims made in connection with inadequate quality of work performed under a contract and is one year. A shortened period is also established by labor legislation - an employee has the right to go to court to resolve an individual labor dispute within three months from the day he learned or should have learned about a violation of his rights, and in disputes about dismissal - within one month from the date of delivery him copies of the dismissal order or from the date of issue of the work book.

In any case, neither the general nor the special limitation period can be changed by agreement of the parties.

At the same time, the limitation period cannot exceed ten years from the date of violation of the right for the protection of which this period was established, with the exception of cases provided for by the Federal Law “On Combating Terrorism.”

Expiration of the limitation period

The limitation period begins to run from the day when the person learned or should have learned that his right was violated. For example, the statute of limitations for compensation for damage in an accident, if the culprit does not have a compulsory motor liability insurance policy, begins to run from the date of the accident itself. But the statute of limitations for compensation for damage from an accident, in the event of insufficient insurance compensation (to make claims against the culprit), begins to run not from the date of the accident, but from the moment the insurance company is notified about it.

For the division of joint property of spouses, the statute of limitations begins to run not from the date of divorce, but also from the moment when the person learned of the violation of his rights.

For obligations that specify a deadline for fulfillment, the limitation period begins at the end of the deadline for fulfillment. If the contract does not specify a deadline for execution or is determined by the moment of demand, the limitation period begins from the moment of demand. For recourse obligations, the limitation period begins from the moment of fulfillment of the main obligation.

Interruption of the limitation period

The limitation period is suspended in the following cases:

If the filing of a claim was prevented by an extraordinary and unavoidable circumstance under the given conditions (force majeure). In this case, the running of the limitation period is suspended provided that the specified circumstances arose or continued to exist in the last six months of the limitation period, and if this period is six months or less than six months, during the limitation period. If the plaintiff or defendant is part of the Armed Forces of the Russian Federation, transferred to martial law; Due to the deferment of fulfillment of obligations established on the basis of law by the Government of the Russian Federation (moratorium); Due to the suspension of the law or other legal act regulating the relevant relationship. Also, if the parties have resorted to a procedure for resolving a dispute out of court provided for by law (mediation procedure, mediation, administrative procedure, etc.), the limitation period is suspended for the period established by law for such a procedure, and in the absence of such a period - for six months from the date of commencement of the relevant procedure.

From the date of termination of the circumstance that served as the basis for suspension of the limitation period, its period continues to run. The remaining part of the limitation period, if it is less than six months, is extended to six months, and if the limitation period is six months or less than six months, to the limitation period.

Claims for which the statute of limitations does not apply

- Requirements for the protection of personal non-property rights and other intangible benefits, except as provided by law;

- depositors' demands to the bank for the issuance of deposits;

- claims for compensation for harm caused to the life or health of a citizen. However, claims brought after three years from the moment the right to compensation for such damage arose are satisfied for the past time no more than three years preceding the filing of the claim, with the exception of cases provided for by the Federal Law “On Combating Terrorism”;

- demands of the owner or other possessor to eliminate any violations of his rights, even if these violations were not associated with deprivation of possession;

- other requirements in cases established by law.

To obtain legal advice and represent your interests in court, call the Lawyer by phone,

Representation is carried out in Moscow, the region and some regions, please contact.

The procedure for recognizing a debt as bad

Only a bailiff who conducts the corresponding enforcement proceedings can recognize a debt as hopeless. This is done in the following order:

- a writ of execution (or other writ of execution) is submitted to the bailiff service for collection;

- the SSP employee carries out all necessary enforcement actions, including searching for accounts and property;

- after a three-year period, if no collections have been made and it has become obvious that the debt cannot be collected, the bailiff recognizes the debt as hopeless.

This is important to know: Calculation of the limitation period under a loan agreement

The creditor has the right to challenge the decision of the Bailiff Service if he believes that the debt can still be collected and the debtor has property that can be collected.

Pay or wait?

As a rule, the last resort is judicial proceedings. But here it is necessary to note one nuance - only those debts for which the statute of limitations has not expired are subject to return through the court. In other words, there is a certain period of time during which the creditor in court has every right to demand repayment of the debt.

Quite often, the majority of unscrupulous borrowers, knowing this feature, do everything possible to “stretch” time and avoid paying the loan in full. Sometimes this can happen during the reorganization of a banking institution, its bankruptcy, or the merger of the bank with other larger companies.

It should be immediately noted that the fact that a bank is “closed” from the financial market does not mean that all obligations under loan agreements will automatically be written off. In such situations, the institution’s loan portfolios are bought by other banks and they will “knock out” all the debt, so it will not be possible to avoid paying the loan.

If you try to somehow avoid paying the debt, this may have a negative impact on the borrower in the future:

- bad credit history

- damaged business reputation and nerves

- various legal proceedings with possible criminal convictions

- sale of property

But anything can happen! No person is immune from ending up in a situation where the financial situation in his life is very unstable. Therefore, he may delay repayment of the loan for years. The debt is growing, and the already difficult life situation is aggravated by calls from collectors.

If we begin to consider the concept of “loan statute of limitations” from the point of view of legislation, then it represents the period during which the lender has the legal right to demand repayment of the loan from the borrower using a lawsuit. Therefore, it is very important to know the legislative framework; if the borrower has full information about the procedures and laws, he can simply delay time and wait for the period when the claim will not be valid. Often the statute of limitations is considered one of the ways to avoid repaying a loan.

Are there statutes of limitations for debt collectors?

It will be much more difficult to resolve the current situation if, in addition to the bank, collectors begin their work. Moreover, the methods they use to collect debts are not always legal and correct. Therefore, if you had to face threats from debt collectors, you need to follow the following tips:

- Contact a lawyer for help

- Write a statement to the police and prosecutor's office

It is always necessary to remember that each borrower, in addition to obligations to the bank, also has its own rights that can be legally defended. One of the rights is the possibility of using the statute of limitations, but there is no need to abuse this. Failure to repay a loan can only be a last resort, and if taken, the borrower may face illegal pressure from debt collectors.

It is best to try to solve financial problems in delicate ways. Sometimes there are situations when the borrower has completely repaid the loan debt, but creditors still sue him. This happens, as a rule, due to technical problems when payments are not processed. Then you cannot do without the help of a qualified lawyer.

What is the statute of limitations for bailiffs for collection?

The statute of limitations for credit debt after a court decision by bailiffs is also calculated at three years. In this case, the writ of execution plays a role. You can apply for recovery according to its contents within the designated period. If this does not happen, it actually loses its power. The countdown date is counted from the moment the court decision enters into force. At the same time, in court it is possible to restore or renew the period of validity of the decision to collect.

This is important to know: Grounds for reinstating a missed deadline for appeal

It’s another matter if the writ of execution was returned by the bailiffs. This can happen for various reasons, most often the impossibility of fulfilling the penalty. In this case, the statute of limitations for debt after the court decision is reset. Over the next three years, the claimant may again submit an application for collection to the bailiff service.

From what time should we count down?

Firstly, it is necessary to understand from what moment these saving three years can be counted. A common mistake is to start counting from the moment the loan agreement expires. This is not true. The bank has its own “safety cushion” in such situations. It is possible that the loan agreement describes a corresponding clause under which the bank has every right to demand payment of the entire amount of the debt if it is determined that the debtor does not fulfill its obligations. The moment when the creditor learned about the termination of payments and exercised his legal right is the starting point for counting three years.

In this case, everything ends well for the debtor. This is ideal. But such a resolution of the problem is only possible if during these three years the borrower has not made any attempts to renew or extend the contractual relationship with the creditor and the bank itself has not done anything to collect the debt from the defaulter.

In fact, this option is far from reality and is more like a fairy tale. No bank will forgive a debt so simply out of the kindness of its heart. In reality the situation is much more complicated. Firstly, the bank can resort to the services of collectors. Secondly, sue. In both the first and second cases, the limitation period is reset to zero, and the countdown begins from the moment of filing a complaint or contacting a collection agency.

And it doesn’t matter what action the bank took to force the defaulter to repay the debt. Every stage is taken into account, even the work of the bailiff. The bank did not turn to the bailiffs and did not file a writ of execution during these three years - great. He does not need the debt, and after three years the life of the debtor becomes wonderful. But in reality, the bank will repeat this action ad infinitum, without crossing the three-year mark. And then the statute of limitations for the loan claim will never end.

When can a debt be written off?

If the bank has already gone to court and achieved a court decision, the chance that it will simply forget about the debt and not contact the bailiff service for forced collection is minimal. Credit organizations rarely go to court immediately; they try to obtain funds by any pre-trial means, often transfer debts to collectors, and go to court only as a last resort. And if it comes down to it, the chance of debt forgiveness is close to “zero.”

But such a possibility can still arise in two cases:

- the decision was made, and within three years the bank either did not receive the writ of execution at all, or received it but did not submit it for enforcement (clause 1 of Article 21 of the Federal Law “On Enforcement Proceedings”);

- the writ of execution was sent to the bailiff service, but no funds were written off from the debtor due to the lack of property, that is, collection was not carried out within three years without the fault of the debtor. In this case, the creditor can withdraw the sheet and submit it again. The period will be re-calculated. Article 43 of the Federal Law “On Enforcement Proceedings” describes all cases when collection can be terminated.

Most often, the following circumstances serve as the reason for termination of enforcement proceedings:

- death of the debtor in the absence of heirs;

- inability to determine where the debtor is located;

- lack of information about material assets belonging to the debtor, as well as if the latter has no income for a long period of time.

In fact, the debt is written off only when it is not possible to collect it.

Commentary to Art. 203 Civil Code of the Russian Federation

1. The commented article provides grounds for interrupting the limitation period. Unlike suspension, the period of limitation is bound by the will of the debtor if there are grounds provided for by law. In such cases, the statute of limitations ceases to flow, and after the specified grounds disappear, it begins to flow again. In other words, the time that passed before the occurrence of the interrupting circumstance does not count towards the limitation period. This makes a break significantly different from a suspension. The grounds for a break are also specific, among which the law includes filing a claim, as well as acknowledging a debt. When considering an application from a party to a dispute about the expiration of the limitation period, the court applies the rules on interrupting the limitation period even in the absence of a request from an interested party, provided that there is evidence in the case that reliably confirms the fact that the limitation period has been interrupted.

It should be borne in mind that the list of grounds for interrupting the limitation period given in Art. 203 of the Civil Code of the Russian Federation and other federal laws (Part 2 of Article 198 of the Civil Code), cannot be changed or supplemented at the discretion of the parties and is not subject to broad interpretation (clause 14 of the Resolution of the Plenums of the Armed Forces of the Russian Federation and the Supreme Arbitration Court of the Russian Federation dated November 12, 15, 2001 N 15/18).

2. Not any appeal to the court is considered as a basis for interrupting the limitation period, but only one that is made in the manner prescribed by law, i.e. in accordance with the requirements of civil procedural legislation.

Of course, it is necessary to comply with the rules on jurisdiction, on the preliminary pre-trial resolution of a dispute in a claim procedure, etc. Consideration of the brought claim usually ends with a decision to satisfy or reject the claim. During the entire period of legal proceedings in the case (until the decision is made and it enters into legal force), the question of the statute of limitations does not arise, since this is devoid of practical meaning. After the decision has entered into legal force and the need for its enforcement has arisen, an independent statute of limitations for the execution of the court decision begins to run.

A civil case accepted for proceedings, however, does not always end in resolution of the dispute. The law provides for a number of circumstances in the presence of which the claim is left without consideration (there are no necessary documents, the claim was made by an incapacitated person, etc.). In these cases, the limitation period is not interrupted, and its course continues in the general manner, since the dispute (as such) was not the subject of judicial proceedings. After eliminating these shortcomings, the plaintiff may bring the same claim in accordance with the general procedure.

The rules of procedural legislation provide for circumstances in the presence of which the court is obliged to suspend the proceedings initiated in the case, as well as those in which the court can do this on its own initiative or at the request of interested parties (a person being in hospital or on a long business trip, searching for a defendant in cases on the collection of alimony and compensation for harm, etc.). In all cases of suspension of proceedings, the limitation period is interrupted at the moment the claim is filed and is not resumed for the entire period of consideration of the case in court of all instances.

3. Recognition of a debt as a basis for interrupting the limitation period is applied to controversial relations, regardless of their subject composition (citizens or legal entities).

Actions indicating recognition of debt are very diverse. Actions indicating recognition of a debt for the purpose of interrupting the limitation period based on specific circumstances may include: recognition of a claim; partial payment by the debtor or with his consent by another person of the principal debt and (or) amounts of sanctions, as well as partial recognition of a claim for payment of the principal debt, if the latter has only one basis and does not consist of various grounds; payment of interest on the principal debt; a change by an authorized person to a contract, from which it follows that the debtor acknowledges the existence of a debt, as well as a request from the debtor for such a change to the contract (for example, a deferment or installment plan); acceptance of collection order. Moreover, in cases where the obligation provided for execution in parts or in the form of periodic payments and the debtor committed actions indicating recognition of only some part (periodic payment), such actions cannot be the basis for interrupting the limitation period for other parts (payments) (clause 20 of the Resolution of the Plenums of the Armed Forces of the Russian Federation and the Supreme Arbitration Court of the Russian Federation dated November 12, 15, 2001 N 15/18). In all such cases, the limitation period is renewed each time for a new full period from the moment the debtor committed the specified actions. However, they must be committed before the statute of limitations expires. If it has expired, then recognition of the debt cannot mean a break in the period, but only indicates the intention of the debtor to voluntarily fulfill the obligation.

Is it possible to claim a debt after the statute of limitations has expired?

Very often you may encounter such a problem as the statute of limitations has already passed, but the borrower continues to demand a refund. It should be immediately noted that such actions of financial institutions are completely illegal. Sometimes a lender may not timely identify the existence of an overdue debt, relying on the borrower’s fear of repaying it. If this happens, then the first thing you need to do is contact a professional lawyer and get quality advice, and then make decisions. Of course, the borrower can be summoned to court. But there is no need to despair right away. A counter-action may be the filing of a petition indicating the expiration date of the limitation period.