The legislation does not provide a list of grounds when the borrower has the right to simply refuse regular payments, so he will definitely have to answer to the bank. Bank employees can send documents to collectors or to court, as well as use other legal means. After receiving the writ of execution, the bailiffs describe the property, apply to withhold part of the salary, restrict travel outside the country and take other measures. However, if certain circumstances occur, the debtor can still be released from forced collection in whole or in part. In this article we will look at the limitation period for a loan and other issues related to this.

- What is the statute of limitations on a loan?

- How long is the statute of limitations for a loan in 2021 and from what point is it counted?

- Limitation period for a loan for a guarantor

- Limitation period for a loan from a deceased borrower

- Statute of limitations on credit card

- When the statute of limitations for a loan debt may be interrupted

- The statute of limitations for repaying the loan to the bank has passed: will the debt be written off?

- What to do if three years have passed and the bank has filed a lawsuit

- Judicial practice on the statute of limitations for loan claims

- What happens if you don't pay at all?

- With what debt will they not be allowed to go abroad?

- What is the best way to pay off a mortgage early with an annuity payment?

- In what cases can a debt not be paid by law?

- What to do if you need to initiate bankruptcy proceedings due to debt problems?

What is the statute of limitations on a loan?

This is the time during which a banking or financial institution can formally file claims in court. In court, the debt is collected not only from the borrower, but also from the legal successor (for example, heir), the guarantor.

After the decision is made, the writ of execution is sent to the bailiffs. If you refuse to voluntarily pay the bank, all possible coercive measures are taken: restrictions on traveling outside the country, seizure of property, inventory and sale of property at auction to pay off the debt, deduction from wages, etc.

Temporary suspension of the limitation period

There are cases when the calculation of the validity period may be suspended:

- If the claim was not filed under force majeure.

- If installment payments have been made.

- If the borrower is serving in a war zone.

- If amendments have been made to legislative acts.

- The participants in the proceedings resolved the conflict independently.

The limitation period may be interrupted if the debtor performs actions that are regarded as agreement with the existing debt. Such actions include:

- The debtor accepted the claims presented by the financial organization.

- Concluding a new agreement with the bank, confirming that the defaulter has acknowledged the debt.

- An application from the debtor to the bank with a request to provide a “credit holiday”, refinancing or restructuring.

- Making payments on debt obligations.

- An in-hand certificate of reconciliation of settlements between the lender and the borrower, certified by the stamp of the credit institution.

Important! The total limitation period, together with all possible interruptions in payments, cannot exceed ten years.

How long is the statute of limitations for a loan in 2021 and from what point is it counted?

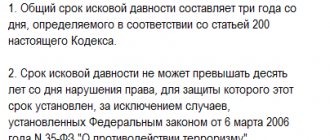

Civil legislation stipulates that the creditor has 3 years to apply to the judicial authorities to collect the debt. There is no consensus among legal experts regarding the start of this period. Some argue that it is worth counting it for each payment made or potential. Others believe that it is better to rely on the end date of the contract. The law states that the three-year interval is counted from the moment the creditor becomes aware of the violated right. It turns out that as soon as the bank learns about the delay according to the schedule, it is recognized as notified. Everything is calculated again for the next period.

Features of calculating limitation periods for receipts

Based on the current one, the validity period of a receipt for a loan of money is three years and is valid in the general manner in the absence of additional circumstances in the case. General conditions include the availability of documentation indicating the fact of concluding a debt transaction, but they do not indicate a specific period. Then the calculation period begins from the moment when the plaintiff claims a violation of the agreement. If the defendant does not pursue the goal of paying off debt obligations in the future, the period is not calculated.

Points related to calculating the statute of limitations on debt obligations deserve special attention:

- When the receipt indicates a specific date for the return of funds, the limitation period is calculated from this date. It is allowed to fill out an application on the day when the money must be returned to the lender

- Some individuals, when filling out a receipt, forget to indicate the exact date of the refund. Then the beginning of the calculation is the date of filing the application for a claim to repay the debt. It is recommended that you make your claim in writing so that it can be used as evidence in legal proceedings if necessary.

If the receipt contains the signatures of both parties, and it is in writing by hand, it has legal force, even if it is not certified by a notary.

Limitation period for a loan for a guarantor

After a delay, the bank will first contact the borrower. If he refuses to make payments or hides, the guarantor is responsible, in cases where he has been appointed. The agreement usually specifies a period after which it ceases to be responsible for the debtor. If the date was not specified, a year must pass after the end of the contract, and in the absence of a claim, no claims will be made. In this case, there is no interruption, there is no possibility of restoring or recounting the time when the guarantor is responsible to the lender.

Bankruptcy of individuals

from 5000 rub/month

Read more

Services of a credit lawyer

from 3000 rubles

Read more

Legal assistance to debtors

from 3000 rubles

more

Write-off of loan debts

from 5000 rub/month

More details

Limitation period for a loan from a deceased borrower

Here the main role is played by what is written in the guarantee agreement. There are several possible scenarios:

- There is no obligation in the agreement to be liable to the lender after the death of the borrower. In this case, all amounts are collected by the bank from the legal successor who enters into the inheritance.

- The guarantor agreed to pay the debt upon death. Even if the relatives of the deceased debtor inherited his property, the guarantor still pays the plaintiff.

Statute of limitations on credit card

In this case, a three-year period also applies. When a person receives a card, as a rule, a payment schedule is not set. However, returns must still be made in certain installments. For example, the agreement may indicate that at least 15% of the borrowed funds must be paid each month by a due date.

If there is a delay, the banking organization will immediately know about it. It is from the first day of non-fulfillment of obligations that the 3 years common to all creditors will begin to run.

When the statute of limitations for a loan debt may be interrupted

Such a combination of circumstances is possible, and the bank receives an advantage. The three-year period will begin to count again, so the creditor will have enough time to protect its rights. Reasons:

- availability of a written application to extend the loan or defer regular payments;

- signing a restructuring agreement, in which the terms are revised, the agreement is extended, and monthly bills are slightly reduced;

- a claim was received from a banking organization demanding the return of money, and in response a letter was sent stating that the borrower does not agree with this;

- other actions indicating agreement with the existence of obligations.

Read Who can declare themselves bankrupt

Thus, after 3 years have passed, the borrower does not need to sign any papers that prove awareness of the presence of delays. Otherwise, the creditor will be able to appeal to the courts legally.

Effect of promissory note

The validity period of the receipt is the period when the document comes into force. This time period is regulated by Article 196 of the Civil Code. During this period, the person who borrowed money receives the right to protect personal interests and go to court. Often people misinterpret the law regarding the limitation period, which deprives them of the chance to assert their rights and return funds.

The money is returned on the day specified in the document. If there is no deadline, funds must be returned after the first official request. The date on which the document was drawn up is not considered the beginning of the calculation of the limitation period, which makes it possible to go to court.

A citizen who borrowed money is obliged to return the funds if:

- a notice has been received requiring you to fulfill your obligations;

- the date specified in the document has arrived.

In the first case, the calculation of the period begins 30 days after receipt of the notice demanding the return of the borrowed funds. This document formulates the claim, indicates the amount of debt and the date by which it is important to fulfill the obligations assumed.

The notice is delivered personally to the person who borrowed the funds. In this case, two copies are prepared in advance. One is handed over to the borrower, and a mark is placed on the second, indicating that the document has been received.

Regardless of the format of the document transfer, the lender is obliged to leave confirmation that the other party was informed of the need to repay the debt within 30 days. If nothing happens during this period, you can safely go to court.

The statute of limitations for repaying the loan to the bank has passed: will the debt be written off?

There is no need to hope that employees of a banking organization will forget about the debt, and it will automatically “burn out” after 3 years. In addition, you can file a claim in court after this period has expired. In addition, the judge can satisfy the claims, and as a result, an inventory of the property in the apartment or house will be carried out. This can be avoided if you use legal means of protecting your rights.

When the creditor does not go to court, he transfers the package of documents to a collection agency. Employees begin to actively work with unscrupulous borrowers: calling, writing on social networks, contacting relatives and friends, colleagues.

Many have heard about the illegal methods that such organizations used to extort money. Fortunately, since 2021 there has been a law on the protection of citizens, which is designed to protect debtors from such schemes. However, these legal entities can still use psychological methods of influence.

Is it possible not to pay on loans after the expiration of the limitation period?

Many people are interested in this question. It should be noted here that bank funds are issued with the condition of their obligatory return. You can't take out a loan and not pay it off. Any banking institution has the authority to claim its funds in court.

If the statute of limitations has passed, the financial institution will not forget about it. Since legal proceedings can no longer be initiated here, the bank will constantly remind you about it. They can even act through relatives.

If the bank cannot recover it, then it is resold to collection agencies. Their methods of work have long been known to everyone. Nothing pleasant. But, however, the law has now been amended to prohibit agency employees from making calls to debtors on weekends and holidays, coming home more than once a week, sending threats and causing harm to health and property.

What to do if three years have passed and the bank has filed a lawsuit

It is possible to send documents to the judicial authorities after the statute of limitations on a loan has expired; there is no article in the law that prohibits such actions. For this reason, the debtor may not be surprised if he unexpectedly receives a summons to appear. The fact is that judges do not independently count how many years the creditor has been inactive; it is the defendant who must point out this fact during the proceedings. It is enough to verbally declare this, referring to Art. 199 Civil Code. In the lawsuit

There are other ways to provide this information:

- draw up a written petition and submit it at the meeting;

- send a registered letter to the court with acknowledgment of receipt;

- give it to the office.

In the latter case, 2 copies are required. The secretary must mark one of the copies as receipt.

Judicial practice on the statute of limitations for loan claims

There are interesting cases when cases ended unexpectedly for both sides of the process:

| Appealing the decision of the court of first instance | Reduced amount |

| Vera took out a loan in April 2010. I paid regularly for 3 months, the last payment was dated July. In November 2015, a summons arrived. The bank filed an application to collect the principal, penalties and interest for the entire specified period. Due to illness, the defendant did not appear, and the claim was satisfied. When filing an appeal, the debtor managed to prove that the deadline had been missed. | Mikhail was sued in October 2021. The debt was calculated from September 2014 to the same month of 2021. The defendant did not agree with the calculations and explained that as of the date of filing the claim, the three-year period had passed. The court decided to recalculate the amount and, as a result, to collect the arrears for the year. |

What happens if you don't pay at all?

If you refuse to fulfill your obligations, you need to be prepared for negative consequences, such as:

- Increasing debt. Not only interest will be added, but also a penalty for each day of delay, penalties and other penalties.

- Damage to credit history. In the future, it will be very difficult or even impossible to get a new loan.

- If not a single payment is made, this may be regarded as fraudulent actions falling under articles of the Criminal Code.

- Imposing restrictions on travel outside the country. Bailiffs have the right to take such measures against debtors, and the debt may not necessarily be multimillion-dollar, 30-40 thousand rubles is enough.

When the bank stops receiving money, employees will start calling the client and sending written complaints to him. Security officers often look for unscrupulous borrowers on social networks, writing not only to them, but also to relatives and acquaintances. This is a psychological impact, and it is impossible to get rid of such pressure even after replacing the SIM card.

The most unpleasant moment is that collectors will call all the numbers they find. Calls will start coming in to family, colleagues, and friends. This is how parents, boss and other persons whom you did not want to notify about this will find out about the failure to fulfill the obligation. Of course, no one will threaten or be rude. The main goal is to get funds into the account, getting on your nerves and causing a feeling of shame.

When the listed methods do not work, the banking organization transfers the documents to the court or collectors (the statute of limitations for a consumer loan or other loan must not expire). In this case, a penalty, state duty, enforcement fee and other costs will be added to the principal debt.

When the court decision comes into force, the bailiffs will come to the debtor’s place of residence and describe the property for further sale at auction and reimbursement to the bank. A writ of execution will be sent to the job, and up to 50% will be deducted from the salary.

Read Credit holidays: what they are, how to apply and terms of provision in 2021

When the borrower is not officially employed, the banking organization will periodically send collection documents to the bailiffs, even upon the arrival of a pension. In such a situation, the Pension Fund is responsible for withholding the amounts.

Experts advise not to bring everything to court. When temporary financial difficulties arise due to job loss, illness or other reasons, it is recommended that you contact the lender directly. Very often it is possible to agree on deferred or installment payments. There is no need to wait for a significant increase in debt and further calls from the security service and debt collectors.

How to calculate the period?

The legislative acts do not precisely define from what period the limitation period should begin. Some lenders count it from the moment the contract expires, while others count it from the moment the last loan payment is made.

Note! If the financial organization decides to close payments early, the statute of limitations will be recalculated. The bank can do this three months after the last payment on the debt.

In most cases, persons against whom proceedings were initiated for debts with an expired statute of limitations win the case. Here they provide a link to the Supreme Court, which indicates that the limitation period begins to count from the moment when the banking institution learned information about the insolvency of the debtor.

Expert opinion

Makarov Evgeniy Sergeevich

Arbitration manager with more than 10 years of experience

In response, lawyers developed new ways to hold the borrower accountable. Now they count this period for each payment and issue claims for each month of delay. However, the final decision is made by the Supreme Court. As a rule, he stands on the side of the creditor.

The limitation period can be suspended in the following cases:

- When amendments are made to the legislative acts regulating this area.

- Force majeure situations.

- Introduction of a moratorium.

- Conscription into the army.

- Declaration of martial law.

The debtor has the right to file a request to change the statute of limitations if, after its expiration, he met with the management of the financial organization. If this is proven, the period will begin from the moment the client visits the bank. In this regard, the debtor must know:

- A meeting here does not mean a telephone conversation unless the conversation itself was recorded.

- CCTV footage is also not evidence of the meeting.

- A receipt for receiving a letter from the bank is also not considered a fact of acceptance of the conditions specified in it.

From what day do you count?

Can financial institutions write off an expired loan? They can, but they do it extremely rarely. As a rule, banks try in every way to recover their funds. Here it is important to understand from what period it is correct to begin counting the statute of limitations.

By credit card

It is important to note that according to the legislation of the Russian Federation, the limitation period here is also three years. But the calculation here will be carried out differently, since plastic does not have a specific end date for lending. The following calculation options are used:

- From the moment of making the final contribution.

- From the date of receipt of notification from the bank about the decision to repay the debt early.

- From the date of cash withdrawal from the plastic card, provided that the card balance was no longer replenished.

By decision of a court

If the existence of a debt is recognized in court, then it must be collected voluntarily or by compulsory means by the bailiff service. There can be no question of a limitation period here, since completely different legal norms are already in force that regulate the process of enforcement proceedings.

For a loan from a deceased borrower

If the borrower is declared dead, then the debt passes to his heirs. The right to transfer debt to other persons applies here.

Note! If the debtor has died, this does not serve as a basis for changing the term or early repayment of the loan.

According to the law of the Russian Federation, inheritance rights occur within six months after the death of a person. During this period, the bank cannot charge penalties for late payments. After the end of six months, the heirs can:

- Enter into inheritance.

- Refuse him.

If persons enter into an inheritance, the limitation period is reset to zero. It begins to count from the moment of receipt of the certificate of entry into inheritance rights.

If citizens have refused the inheritance, then the banking institution does not have the authority to demand even close relatives to repay the debt. And the statute of limitations will continue to count after the break. But banking institutions rarely leave such situations. They will try to collect debts by all means. Actions of creditors:

- Presentation of financial conditions to the executor of the will.

- Submitting a statement of claim to the court to recover debts from inherited property.

It is important to note that only refusal to enter into inheritance rights serves as a reason for ignoring debt repayment requirements.

For guarantors

It is important to note here that if the loan agreement does not reflect the start and end dates of the guarantee period, then by default it is valid for one year after the termination of the contract period.

Expert opinion

Makarov Evgeniy Sergeevich

Arbitration manager with more than 10 years of experience

If the financial organization makes claims against the guarantor during this period, then he is obliged to fully compensate for all damages. If the statute of limitations has passed, then neither the court nor the banking institution has the authority to temporarily terminate, restore or start new deadlines. It is not the period itself that expires here, but the loan agreement.

Note! If a financial institution, during the validity of the contract, changed the interest rate on loans without obtaining the consent of the guarantor, then such a contract is considered invalid. Therefore, it is important not to sign any documents after the lender and borrower have entered into an agreement.

If the debtor is declared dead, the guarantor can:

- Continue to fulfill the requirements under the contract, if so provided for in it.

- The guarantee is transferred to the heir if this is also specified in the contract.

With what debt will they not be allowed to go abroad?

If a person owes 30 thousand rubles. and moreover, he is unlikely to be able to leave the territory of the Russian Federation, since the contractor will impose restrictions on leaving the country. The corresponding resolution is sent to the Border Committee. The validity period of such a decision is six months. If the debt is not repaid during this time, a new restrictive document is prepared.

However, even with a smaller amount it is possible to restrict the debtor’s movements. If the debt is 10-30 thousand rubles and a writ of execution is received, the bailiffs are given 5 days for voluntary settlement with the creditor. If a person is still inactive and does not make payments, after 2 months you can prohibit him from traveling abroad. This amount consists of various debts collected in court.

Is it legal to transfer debt to collectors?

Even if the statute of limitations on a loan from an individual or legal entity has expired, the bank can, without any obstacles, submit documents for debt collection by collection organizations. This is a normal practice that has been used for many years. Most lenders turn to third-party collectors as early as possible.

Some visitors to forums on the Internet point out the illegality of such actions due to a violation of banking secrecy. It all depends on the documentation that was signed when concluding the contract. The borrower, by signing, agrees that personal information about him may be transferred to third parties. After July 1, 2014, the following rule applies: upon receipt of any loan, the borrower automatically agrees to the transfer of materials to interested parties. The documents should not contain a direct prohibition on such actions.

Bankruptcy of individuals

from 5000 rub/month

Read more

Services of a credit lawyer

from 3000 rubles

Read more

Legal assistance to debtors

from 3000 rubles

more

Write-off of loan debts

from 5,000 rubles/month

More details

If you suddenly discover that the debt was transferred to collectors illegally, you need to complain to Roskomnadzor:

- go to the official website rkn.gov.ru;

- select “processing of personal data” in the subject of the appeal;

- fill out the form that opens;

- attach supporting documentation, including audio recordings of conversations with collection agencies, messages in instant messengers, etc.;

- Enter the security code and click “send”.

How long is a debt receipt valid?

The validity period of a receipt from the debtor is regulated on the basis of Article 196 of the Civil Code. This concept refers to a set period of time during which the document comes into legal force. At this time, the citizen who loaned the money has the right to initiate legal proceedings. LID (statute of limitations) controls the validity of the receipt. Today this time is limited to three years.

Often, citizens incorrectly interpret the established procedure by law, which is why they cannot fully defend their right to return lost funds.

Calculation is impossible from the first day in the following situations:

- If the agreement was established verbally

- Conclusion of an agreement confirming the oral procedure for financial cooperation

- Transfers of funds between individuals.

Article 200 of the Civil Code establishes the right of calculation from the moment the lender learns of the offense committed. In this situation, the main position of the creditor is to return his money within the time frame that was specified during the agreement process.

In accordance with the issued receipt, the return must be made:

- On a set date, which must be fixed in the document

- When no date is specified, refunds will be made upon formal first request.

After the first demand, when no return occurs, such actions may be qualified as an infringement of creditor rights.

In what cases can a debt not be paid by law?

There are no grounds in the law for which it is possible to completely waive obligations under a loan agreement. If you suddenly come across an advertisement on the Internet from a company that offers to cancel payments for a small fee, it is better not to respond. However, the legislator has provided for certain cases when the situation for the debtor is such that he is exempt from collection:

- The statute of limitations for claims on the loan has expired. In this case, the court must officially refuse the financial organization to initiate proceedings in the case for such a reason.

- The funds were written off by the bank as a bad debt. Such situations occur infrequently, because it is much easier to resell a problem asset, especially since he is not obliged to send documents for write-off.

- The debtor entered into an agreement with the creditor to repay part of the amount, and the remainder is then written off.

- An insured event occurred with a valid policy. The document states that the remaining debt is paid by the insurer. For example, this may be provided for when the borrower becomes disabled. He is required to independently send written notification of the incident. The company will send to the debtor a list of necessary documents and indicate the procedure for settlement with the bank.

The statute of limitations for claims on loans is 3 years. Under certain circumstances, it can be interrupted, restored and counted again. If the three-year period is missed, the bank still has the right to go to court and collect the unpaid amounts along with penalties. The debtor is obliged to react in time and declare to the court that time has been lost, and nothing more should be demanded from him.

What to do if the deadline expires and the debt is not repaid.

If you are not given the money on a receipt, then in addition to the statute of limitations, it is advisable to make sure whether the receipt will be valid if you go to court, and whether your receipt is evidence of the loan. After all, an invalid cash receipt in court will bring a lot of trouble to its owner.

Whether the receipt has legal force can be checked as follows:

Considering that the receipt is a form of a cash loan agreement, the text of the receipt must necessarily contain the following data:

- about the lender;

- about the borrower;

- about the loan amount.

If the above three points are in your receipt, then you can be sure that the receipt has legal force and will be evidence in court.

A proper promissory note may also contain:

Articles on the topic (click to view)

- The Supreme Court corrected the courts in the case of a “consumer” fine

- Bankruptcy procedure for an individual: steps, stages, step-by-step diagram

- Consequences and restrictions for the debtor and his relatives during bankruptcy proceedings under 127-FZ

- 159 Federal Law on additional guarantees for social support for orphans

- Phips open registers trademarks

- Federal Law on Insolvency (Bankruptcy) of Individuals 127-FZ and 154-FZ: what you need to know

- What is payment confirmation? Payment confirmation document

- loan term and date of repayment;

- the amount of interest for using the loan;

- other conditions that do not contradict the legislation of the Russian Federation.

It is better to have a handwritten receipt. Since a printed receipt is fraught with some dangers from cunning debtors. If it is important for someone to know such details, please ask a question in the comments.

Whether witnesses participated in drawing up the receipt or whether the receipt was drawn up without witnesses does not matter. That is, if there is a receipt, then witnesses will never be superfluous.

But if the receipt was not drawn up, then the witnesses will not be able to replace it. The court will not accept witness testimony as evidence of the loan.

I advise anyone who borrowed money without a receipt to read about how to repay a debt without a receipt.

Repayment of a debt by receipt can be a lengthy and useless procedure until the creditor decides to go to court. An application to the court on a receipt can be submitted in a simplified manner by paying only half of the required state fee and completing the process of obtaining a court decision in literally one week.

Collection of funds against a receipt in court occurs with almost one hundred percent probability. It should be noted that if the debt on the receipt was repaid, then the borrower himself must prove this.