When an employer receives a writ of execution against an employee, the document must be accepted and processed by a specially appointed employee, most often a payroll accountant. First, he must register it and then calculate the total indicators according to the writ of execution for deduction from the employee and transfer them according to the specified details. In addition, your employee will have to interact with government agencies on issues related to these documents.

Enforcement documents provide for a variety of penalties - alimony payments, debts on credit obligations, utility bills, compensation for damage caused to third parties, etc. To correctly withhold amounts under the current legislation of the Russian Federation, it is necessary to understand in detail the features and nuances that arise when resolving an issue of this kind.

The 1C:ZUP program has a special document for deductions based on writs of execution.

Legislation on executive documents

According to Art. 137 of the Labor Code, deductions from wages may be made in cases regulated by the Labor Code or specific federal laws. The amount of such withholding should not be more than 20%, and in some situations (according to specific regulations) - no more than 50%.

There are also situations in which the amount of withholding will not exceed 70%, for example, the collection of alimony payments, compensation for harm or damage. With this option, deductions are made regardless of how the employee feels about it. The main thing is that an official document from government agencies must be drawn up.

If the employee himself expresses his will to withhold any amount or percentage from his wages, then in this case the norm of labor legislation does not apply. In other words, there is no restriction on how much an accountant has the right to withhold a specific amount of money from an employee's salary.

Important! An official withholding document received by an organization has more legal force than a statement from an employee. In this regard, deduction should initially be carried out according to an official document from government agencies, and then by decision of the individual himself.

Start of hold

At the initial stage, when processing a writ of execution, a specialist may encounter specific difficulties - at what point should deductions be made and how to determine the amount of debt under the document. The moment the retention begins is the date the company receives this document.

For example, if it was received by the employer in early October before the payment of the September salary, then the deduction must already be made from the salary for September. If the document is received by the company after the payment of the September salary, then the first deduction will be made from the salary for October.

When withholding, you also need to pay attention to whether it indicates a specific start date for the document. In many cases, bailiffs, as a rule, independently indicate the amount of debt. In a situation where an executive document is received by an organization much later than the specified start date of withholding, the accountant does not need to recalculate anything - he uses the figure indicated in the document from the date when the document came into his hands.

If the company is not sent a writ of execution, but, for example, a notarized agreement or a court order, then the accountant must act differently. With this option, he will have to independently determine the amount of debt, since a specific figure is not indicated in the document. For example, it may be formalized that alimony payments in the amount of 25% should be withheld from income. And then the accountant independently determines the amount depending on the employee’s income. In this case, the moment the retention begins will be the date specifically indicated in the document.

Before accounting

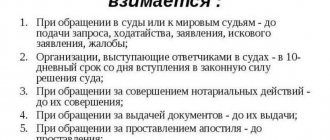

As a general rule, registration of a writ of execution can occur the next day after its receipt. Although there is no point in delaying the executive documents so much. It is difficult for the HR department or accountant to competently verify the authenticity of the executive document, as well as documents identifying the identity and authority of the person presenting it. Therefore, in medium and large companies, the function of interaction with external collectors is assigned to the legal department or a specially authorized security officer, which is quite justified. It is these specialists, acting more consciously, who should have the right to certify (sign) the note on receipt of the writ of execution.

The fraudster, as a rule, applies to a regional court of general jurisdiction with a statement of claim under a “fake” agreement, the amount of which does not exceed 500,000 rubles. This is the threshold for disputes for an amount below which decisions by magistrates are made in a simplified manner within the framework of a court order in accordance with Article 121 of the Code of Civil Procedure of the Russian Federation. The simplified procedure allows the magistrate alone, on the basis of an application for the recovery of a sum of money, to issue an order without a trial as such and without summoning the parties to hear their explanations.

To obtain a contract form, details and a sample seal, fraudsters deliberately enter into fictitious contractual relationships and conduct business correspondence in order to obtain the necessary data. Tour operators are especially vulnerable, since they can send their contract by email to any counterparty.

The next stage is the theft itself. The claimant comes to the bank with a writ of execution, or more often sheets (each worth less than 500,000 rubles), which the bank is obliged to execute within one day, if there is no doubt about its authenticity. After which the funds leave the legal entity’s account to the fraudster.

Withholding limits

When calculating the amount of deduction, the accountant must focus on the limits regulated by law:

- up to 50% - in general cases;

- up to 70% - in exceptional cases.

Exceptional cases include alimony payments; compensation for harm caused to the health of another person; compensation for harm to individuals who suffered damage due to the premature death of their breadwinner; compensation for damage caused due to a criminal act.

However, in practice, questions often arise about exactly how much deduction should be made on a document. This is especially true in situations where one employee receives several enforcement documents at once. In this case, the payroll accountant must evaluate which of the documents received is more important, i.e. draws attention to the order of satisfaction of requirements under executive documents.

The first priority includes the exceptional situations listed above, as well as compensation for moral damage. Further, the requirements are distributed according to the degree of importance and, for example, the bank’s demand for collection of loan debt falls into the fourth stage.

As a result, it turns out that first it is necessary to satisfy the requirements related to the first stage. If possible, funds are withheld according to requirements from the following queues - second, third, etc.

What is the maximum amount they can withhold?

The entire amount of salary or other income received by the debtor cannot be withheld on the basis of a writ of execution. Restrictions on withholding money are specified in No. 229-FZ. The bailiff does not independently determine the amount of collection; it is indicated in the enforcement documents (the exact amount or share of the salary).

The maximum amount of deductions is regulated by Art. 99 No. 229-FZ, it cannot exceed :

- 50% of wages or other income under one writ of execution;

- 50% of earnings under several writs of execution.

Funds to repay the loan debt begin to be withheld immediately after receiving the writ of execution (from the next salary payment).

The maximum amount of recovery is calculated from the amount remaining after all taxes have been withheld from the employee. In some cases, the amount of recovery can reach 70% of all income received by the debtor. This is possible in accordance with the rules prescribed in Part 3 of Art. No. 229-FZ (collection of debt for alimony, in connection with death due to the fault of the debtor, compensation for harm caused to health, etc.)

Procedure for working with writs of execution

The organization receives a wage foreclosure filed by employees of the bailiff service. The following documents are attached to it:

- copy of the writ of execution;

- resolution on withholding the enforcement fee;

- account details with a credit institution for transferring withheld amounts.

When receiving a deduction from wages, you need to do the following:

- register the document in a special journal, the form of which can be developed by the company independently;

- fill out and send the tear-off spine to the bailiff. This action will prove that the writ of execution was received by the organization and accepted for execution;

- it is obligatory to familiarize the employee for whom the writ of execution has been received with its contents against signature;

- provide the payroll accountant with the recorded withholding order;

- keep the received document until it is returned to the bailiff.

In terms of organizing the document flow of executive documents, the legislation does not clearly indicate how exactly it should be carried out. However, if the document is lost or it is untimely returned to the bailiffs, for example, upon dismissal of an employee, then a fine will be imposed on the company and its officials in accordance with Part 3 of Art. 17.14 of the Code of Administrative Offenses of the Russian Federation, namely for the employer from 50 to 100 thousand rubles. and for responsible persons from 15 to 20 thousand rubles. The same administrative penalty is provided if, according to the executive document, the specified requirements for withholding and transferring funds are not fulfilled.

Control over the processing of writs of execution is assigned to bailiffs. They have the right to conduct inspections in companies to which enforcement documents have been sent to employees.

Important! In order to protect the organization from penalties, it is advisable to properly organize the recording and storage of writs of execution. You should also appoint responsible persons who will register, store and execute documents.

How much can be deducted from your salary if you have children?

How much bailiffs can deduct from wages is regulated by law and depends on the nature of the debt, as well as a number of other nuances. For example, on whether the debtor has minor children.

The minimum amount of deductions is most often 20% of salary, and the maximum is 50%.

But there may be exceptions.

The legislation establishes restrictions on the maximum amount of deductions from wages that bailiffs can make. The size of these restrictions is influenced by the presence of minor children and some other factors.

So, for example, you can deduct from the salary of a person who does not have children in the following amounts:

- Based on the law - no more than 20% of the salary;

- Based on federal law or by court decision - no more than 50% of the salary;

- As an exception (the most common example is alimony) - no more than 70% of the salary.

For a person with children, the maximum deduction amounts are lower:

- If you have 1-2 children - no more than 30% of the salary;

- If you have a child studying at a university on a commercial basis - no more than 30% of the salary;

- In the event of the death of a spouse and the presence of minor children - no more than 25% of the salary;

- In the event of the death of a spouse in the absence of minor children - no more than 50% of the salary.

It is categorically unacceptable to write off 100% of your salary to pay off debt!

Example of calculation of deductions

Let's consider an example of calculating deductions for two executive documents received by the employer in relation to one employee.

First Spanish sheet - on withholding child support payments in the amount of 25% of wages.

Second Spanish sheet - about withholding debt under a loan agreement in the amount of 50% of the salary, which is equal to 15,000 rubles.

For October 2021, the employee received a salary of 25,000 rubles. He has the right to receive a standard tax deduction - 1,400 rubles. for a minor child.

The accountant must make the following calculations:

- Personal income tax = (25,000 - 1,400) * 13% = 3,068 rubles.

- 1 sp. sheet = (25,000 - 3,068) * 25% = 5,483 rub.

- 2 Spanish sheet = (25,000 - 3,068) * 50% = 10,966 rub.

However, according to the second Spanish According to the document, the amount should be withheld in a smaller amount, since it is necessary to take into account the deduction under the first application. document:

- (25,000 - 3,068) * 50% - 5,483 = 5,483 rubles.

Residual debt under the second application. the document will need to be withheld in the following months in the same way, that is, after alimony is withheld.

Holding Features

When making deductions from wages, you need to pay attention to the following nuances:

- withholding cannot apply to certain types of income, for example, state benefits or financial assistance from the federal budget, certain types of compensation payments, etc.;

- the fee for transferring money may be withheld from the employee in respect of whom this procedure is being carried out. This can be either a commission from a credit institution for processing a payment order or costs for transfer by mail. The percentage limitation established by law does not apply to these amounts;

- when a new requirement is received, the document is taken into account along with previously received ones, i.e., it is not postponed until the previous withholding requirements are fully satisfied;

- bailiffs can check how deductions are calculated, either on their own initiative or on the basis of a complaint from the claimant.

Features of deduction from a salary card

Many organizations pay wages to their employees using salary cards. The available funds on such cards from the debtor, by order of the bailiff, can be directed to the benefit of the creditor. Also, based on the bailiff’s order, the accounting department calculates the amount that is withheld from the employee’s salary, and the remaining funds are transferred to the citizen’s card. The amount of collection may be withheld in favor of the recipient of the debt in full, as the property of the debtor.

Paragraph 4 of Article 99 No. 229-FZ defines only one exception to this rule, which limits recovery from the debtor’s salary accounts. The debt cannot be written off only based on the last periodic salary payment. This means that the amount of money on the salary card can be written off in full, except for the last salary payment, until the next time it is received into the account.

There are cases when bailiffs send an order to deduct from wages according to a writ of execution not to the accounting department, but to the bank. In this case, the latter will withhold 50% of the salary upon each receipt. And with each subsequent one, the funds that were in the account before the salary (advance) was transferred will be written off in full.

Automation of accounting

To automatically process writs of execution in 1C, you must first configure the program, namely, check the box that requires deductions to be made on writs of execution. In this case, automatic calculation of deductions will be made in accordance with the entered requirements for each document.

Then you need to set up a list of payments that will participate in the formation of the base for deduction under executive documents. The list can be adjusted depending on what is indicated in the company’s local documents.

To enter information on a specific writ of execution in 1C, use the tab associated with deductions. In the document being created, you must indicate all the important conditions contained in the executive document. Based on the information entered, you can generate a registration card for the executive document. Information on all cards goes into a special journal for recording executive documents.

Direct deduction according to executive documents is carried out on the basis of a salary calculation operation. The accountant has the opportunity to disclose information and check the correctness of calculation of the amounts of deductions for a specific month of calculating wages to an individual.

How to accept and register

If the theater, as we know, begins with a hanger, then work with the executive document begins with its reception and registration. Let's dwell on this in more detail. Most often, a company receives writs of execution addressed to its employees (for the payment of alimony, administrative fines, etc.), for the execution of which the employer must make deductions from their wages. Much less often, an organization receives writs of execution addressed to itself - their “working out” is usually first dealt with by the legal service, which conducts litigation. After all, in ordinary language, a writ of execution is the result of a case lost in court. The writ of execution is issued by the court after the judicial act enters into legal force.

note

Such a safety net is quite justified, since recently various types of scammers have become noticeably more active, stealing funds from the bank accounts of legal entities with the help of writs of execution issued by the courts. Large companies whose accounts are opened in large banks are chosen as victims. After all, the large volume of transactions both in the company and in the bank makes it difficult to promptly track illegal withdrawals of funds from bank accounts.