Legislation on labor leave.

While expecting a baby, an employee is given one of the following types of leave:

- for pregnancy and childbirth;

- newborn care;

- regular labor;

- without saving your earnings.

Art. 115 of the Labor Code of the Russian Federation states that an employee has the right to leave, which must be paid, for the year worked. Its duration is 4 weeks.

For some groups of workers, the rest period is extended. Additional days are provided on the basis of the Collective Agreement or other local acts adopted by the company.

Labor legislation states that an employee can take advantage of the right to paid rest as early as 6 months after employment.

But the Labor Code (Article 260) says that a woman expecting a baby can take leave before issuing a certificate of incapacity for work according to the BiR, regardless of the time worked.

If necessary, the employee can postpone the rest time to dates after the end of the maternity bulletin.

At the same time, compensation for unused vacation for the year is not paid. The legislation states that employees must rest (at least 28 days) during the calendar period for which this is provided.

What payments are due to pregnant women in 2021: working, unemployed, students.

Taxation of compensation for unpaid leave

If you look purely at the adopted amendments to the Labor Code of the Russian Federation in 2014, you will notice that compensation is now subject to many taxes, namely FFOMS (Federal Compulsory Medical Insurance Fund), TFOMS (Territorial Medical Insurance Fund), FSS (Social Insurance Fund) , NSiPZ (accidents and occupational diseases).

As you can now see, you will need to give a significant percentage of the entire amount in general, which greatly reduces the initial value. However, all this is mandatory taxation and there is no escape from it.

How to receive compensation for unused vacation.

Compensation for unused maternity leave can be issued only in two cases:

- upon termination of an employment contract;

- if the required rest period is more than 4 weeks.

In the second case, compensation can only be paid partially, for additional vacation days, if the employee is entitled to them.

Replacing rest time with a cash payment is not the employer’s responsibility, so he can provide the employee with full vacation and pay for it.

Upon dismissal from the company, an employee will be able to receive the following types of benefits:

- earnings for the period actually worked;

- vacation compensation;

- dismissal benefits, if required in accordance with legislation or local regulations.

However, termination of an employment contract entails the termination of all relations with the employer.

This method is usually used if compensation is needed for unused leave after maternity leave, and the woman does not plan to return to her old duty station.

Dismissal after maternity leave: how to calculate compensation for vacation

The employee was on maternity leave for up to 1.5 years. She decided to quit without going to work. How to calculate monetary compensation if the employee did not actually work during the billing period? What should be taken as average earnings?

Cash compensation is paid to the employee upon dismissal for all unused vacations in accordance with Art. 127 Labor Code of the Russian Federation. Based on clause 28 of Rule No. 169[1], upon dismissal of an employee, compensation for unused vacation is calculated in proportion to the time he worked in the institution.

Vacation days for which compensation must be paid are calculated in proportion to the months worked in accordance with clause 35 of Rule No. 169, starting from the date of hire, with the days worked being:

- less than half a month - discarded;

- more than half a month is counted as a full month.

Therefore, to determine the number of vacation days not used by an employee that are subject to compensation upon his dismissal, the employer needs to determine:

- total length of service in the institution;

- the presence of periods excluded from the length of service giving the right to leave, their duration in calendar days;

- the number of vacation days due to an employee upon dismissal;

- the number of vacation days used by the employee at the time of dismissal.

The length of service giving the right to leave is calculated as the difference between the employee’s total length of service in the institution and the periods not included in the leave length of service.

Article 121 of the Labor Code of the Russian Federation establishes that the length of service that gives the right to annual basic paid leave includes:

- actual work time;

- the time when the employee did not actually work, but in accordance with labor legislation and other regulatory legal acts containing labor law norms, a collective agreement, agreements, local regulations, an employment contract, he retained his place of work (position), including the time of the annual paid leave, non-working holidays, weekends and other rest days provided to the employee;

- time of forced absence due to illegal dismissal or suspension from work and subsequent reinstatement to the previous job;

- the period of suspension from work of an employee who has not undergone a mandatory medical examination (examination) through no fault of his own;

- the time of unpaid leave provided at the request of the employee, not exceeding 14 calendar days during the working year.

The length of service giving the right to annual paid leave does not include the time:

- absence of an employee from work without good reason, including due to his removal from work in cases provided for in Art. 76 Labor Code of the Russian Federation;

- leave to care for a child until he or she reaches the legal age.

Based on Art. 139 of the Labor Code of the Russian Federation, the average salary of an employee is calculated based on the salary actually accrued to him and the time actually worked by him for the 12 calendar months preceding the period during which the employee retained his average salary. To calculate the average salary, all types of payments provided for by the remuneration system and applied by the relevant employer are taken into account, regardless of their sources. The procedure for calculating average wages is approved by Regulation No. 922[2].

Clause 5 of Regulation No. 922 defines periods, as well as amounts accrued during this time, that are excluded from the calculation, for example, when an employee:

- received average earnings in accordance with the legislation of the Russian Federation, with the exception of breaks for feeding the child;

- received benefits for temporary disability or maternity benefits;

- was released from work with full or partial retention of wages;

- was on leave without pay (parental leave until the child reaches the age specified by law).

In connection with this, Regulation No. 922 established a special procedure for calculating average wages in cases where the employee did not actually have accrued wages or actually worked days for the billing period:

- for a period exceeding the billing period, or if this period consisted of time excluded from the billing period in accordance with clause 5 of Regulation No. 922. Average earnings are determined based on the amount of wages actually accrued for the previous period, equal to the billing period (clause 6 of Regulation No. 922);

- for the billing period and before the start of the billing period. Average earnings are determined based on the amount of wages actually accrued for the days actually worked in the month of occurrence of the event that is associated with maintaining average earnings (clause 7 of Regulation No. 922);

- for the billing period, before the start of the billing period and before the occurrence of an event that is associated with maintaining average earnings. Average earnings are calculated based on the tariff rate and salary (official salary) established for the employee (clause 8 of Regulation No. 922).

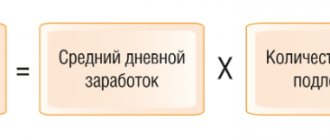

According to clause 10 of Regulation No. 922, when paying compensation for unused vacation, the average daily earnings are used, which is calculated by dividing the amount of wages actually accrued for the billing period by 12 and by the average monthly number of calendar days (29.4).

Compensation for unused vacation is issued to the employee on the day of dismissal or the next day after applying for payment in accordance with Art. 140 Labor Code of the Russian Federation.

Thus, if the employee did not have actually accrued wages and actually worked days for the billing period and before the billing period, the average earnings are calculated based on the wages accrued for the actually worked days in the month of occurrence of the event that is associated with maintaining the average earnings (clause 7 of Order No. 922), that is, for the calculation, the actually accrued wages and the time worked up to the day of registration of maternity benefits are used, since the period during which the actually worked period and, accordingly, the accrued wages can be taken for calculation is legislatively is not limited. The law establishes that the billing period is taken into account from the date of hiring.

Example

The employee was hired on 09/01/2010, maternity benefits were accrued from 11/01/2010 to 03/20/2011, since 03/21/2011 the employee has been on maternity leave for up to 1.5 years. The monthly salary is 10,000 rubles, there were no other accruals, the period from 09/01/2010 to 10/31/2010 was fully worked out. The employee quits on April 28, 2012 without returning to work. The next vacation is taken at the rate of 28 cal. days

During the billing period of 12 calendar months before the day of dismissal from 04/01/2011 to 03/31/2012, the employee was on maternity leave and had no actual accrued wages; in the previous period from 04/01/2010 to 03/31/2011, the time worked was from 09/01/2010 to 10/31/2010, therefore, we accept for calculation this period and the wages actually accrued for this time.

To calculate vacation days, we take the period from 09/01/2010 to 03/21/2011, which is 7 months (the period from 03/01/2011 to 03/21/2011 is 21 days, in accordance with clause 35 of Rule No. 169, the number of days that are more than half a month, counts as a full month.

- The number of days of unused vacation is 16.33 (28 calendar days / 12 months x 7 months).

- To calculate average earnings, we take the salary calculated for the period from 09/01/2010 to 10/31/2010 - 20,000 rubles. (RUB 10,000 x 2 months).

- We find the average daily wage: 340.14 rubles. (RUB 20,000 / 2 months / 29.4 cal days).

- Compensation for unused vacation will be 5,554.49 rubles. (340.14 rub. x 16.33 cal. days).

note

In accordance with clause 16 of Order No. 922, when an institution increases tariff rates, salaries (official salaries), in this situation, the average salary of an employee, calculated for the billing period, increases by indexing it by the increase factor. This is due to the fact that the increase occurred after the calculation period before the occurrence of the calculation of average earnings associated with the calculation of compensation upon dismissal.

If the employee did not have a worked period before the occurrence of an event related to the preservation of average earnings (clause 8 of Procedure No. 922), the tariff rate and salary corresponding to the position occupied by the employee in accordance with the staffing table (tariffication) approved for the year are accepted for calculation. , which calculates the average earnings associated with dismissal.

Example

The employee was hired on October 13, 2010 as a secretary. On 10/14/2010, she submitted a sick leave certificate in connection with temporary disability, which was open for the period from 10/13/2010 to 11/01/2010, and from 11/02/2010 to 03/21/2011, a sick leave certificate was opened in connection with pregnancy. From March 22, 2011, the employee was granted maternity leave for up to 1.5 years.

During the billing period of 12 calendar months before the day of dismissal from 04/01/2011 to 03/31/2012, the employee was on maternity leave and had no actual accrued wages; in the previous period from 04/01/2010 to 03/31/2011, she also did not have any time worked and actually accrued wages.

Compensation for unused vacation is calculated for 6 months, since the period from 10/13/2010 to 10/31/2010 is 19 calendar days, from 03/01/2011 to 03/21/2011 – 21 calendar days. They are rounded to full months (clause 35 of Rules No. 169).

- The number of days of unused vacation is 14 (28 calendar days / 12 months x 6 months).

- In this case, for calculation we accept the official salary of the secretary in accordance with the staffing table of the institution for 2012, for example, 15,000 rubles.

- We find the average daily wage: 510.2 rubles. (RUB 15,000 / 29.4 cal days).

Compensation for unused vacation will be 7,142.8024 rubles. (510.2 rubles x 14 cal days).

[1] Rules on regular and additional leaves, approved. NKT of the USSR dated April 30, 1930 No. 169.

[2] Regulations on the specifics of the procedure for calculating average wages, approved. Decree of the Government of the Russian Federation dated December 24, 2007 No. 922.

I. I. Shklovets - expert of the journal “Explanations of executive authorities on the conduct of financial and economic activities in the public sector”

Accounting for compensation for unused vacation

The accounting is carried out absolutely identical to many other accountings, since the main meaning is the same everywhere - this is to calculate as accurately as possible the possible value of a particular action or coefficient. If this is done with high accuracy, we can say that you have a fairly skilled accountant who knows his business firsthand.

If you look purely at the technical side, then everything seems much easier than from the outside, since the same formulas are used from generation to generation, but you also need to be able to use them.