The concept of offset or refund of overpaid tax and the reasons for the overpayment

Offsetting the amount of overpaid tax is a special procedure provided for by the current legislation of the Russian Federation, which consists of confirming the existence of an overpayment and the subsequent distribution of excess financial resources.

The payment of tax will be considered both a direct transfer of funds in a certain amount to the state budget account, and the offset of the excess amount by the authorized tax authority.

The offset or refund of overpaid taxes, fees, penalties, and fines is based on the principles of the current tax legislation of the Russian Federation and is aimed at preserving the interests of taxpayers.

Practice shows that overpayments can occur even among the most experienced and attentive accountants. The most common reasons for its occurrence are as a result of filing an amended return for certain tax periods.

If the amount in the new declaration is less than the original document, an overpayment occurs.

In addition, overpayments often arise for simpler reasons - mechanical errors of authorized persons, clerical errors, inaccuracies, failure to comply with established deadlines for filing tax documents, errors in the formation of the tax base, etc.

A possible reason for an overpayment may also be certain changes in tax calculations that were introduced by the current legislation of the Russian Federation after the first declaration had already been submitted to the tax organization.

Decision on crediting overpaid tax

Article 78 of the Tax Code of the Russian Federation regulates that a decision to offset the amount of overpaid tax can be made by the authorized body if there are appropriate grounds. This decision must be created within a 10-day period from the day on which the interested party submitted the corresponding written application.

The offset of overpaid tax is carried out at the place of registration of the taxpayer, without accruing any interest on this amount, unless Article 78 of the Tax Code of the Russian Federation establishes other rules and regulations.

An important nuance when offsetting an amount of a certain amount that was overpaid will be the fact that Article 78 and its provisions can only be applied if the overpayment was the result of the actions of the taxpayer alone.

In situations where additional funds were transferred due to the need to fulfill any order or decision of the tax authority, the funds cannot be offset.

Before the immediate moment of making a decision on the offset of funds, the authorized body is obliged to check and reconcile all available data to confirm or refute the need for offset.

In cases where evidence of the need has not been identified, the taxpayer receives an official refusal to offset funds, indicating the reasons and grounds for this decision.

Reimbursement of overpaid personal income tax

When does an overpayment of personal income tax occur?

A direct prohibition on paying personal income tax at the expense of an agent is specified in clause 9 of Art.

226 of the Tax Code of the Russian Federation: “Payment of tax at the expense of tax agents is not allowed, except in cases of additional assessment (collection) of tax based on the results of a tax audit in accordance with this code in the event of unlawful non-withholding (incomplete withholding) of tax by a tax agent.” An overpayment of personal income tax may occur in the event that a tax agent excessively withheld and transferred to the budget tax on amounts of income paid to an individual. Situations in which tax may be over-withheld are as follows:

• The employee received leave in advance and quits. Upon dismissal, the employer may withhold part of the overpaid vacation pay from the income due to the employee, but not more than 20%. The employee can return the rest voluntarily (this is where the over-withheld tax will appear).

• If an error is made when calculating sick leave benefits and the employee is paid an inflated amount of benefits, the Social Insurance Fund will not accept such amounts for credit. You will have to recalculate benefits and personal income tax. Again, the excess paid will either have to be withheld from income (but only in case of a counting error), or the employee will have to be asked to voluntarily return the funds.

• When an employee is entitled to standard tax deductions, but he did not provide supporting documents in a timely manner. It is necessary to recalculate the tax base for personal income tax from the beginning of the year, and an over-withheld amount of tax may arise.

• If the employee receives a property deduction not from the beginning of the year. It will be necessary to recalculate the employee’s income from the beginning of the year and return the excess tax withheld.

• If the organization has a foreign employee working under a patent, then the previously withheld personal income tax will have to be returned when notification of the right to reduce personal income tax on his income by the amount of fixed advance payments was received from the tax authority after the employer began paying income to the employee.

• When personal income tax is incorrectly calculated at a higher rate or tax is withheld from non-taxable income.

How to identify an overpayment

The amount of personal income tax that is excessively withheld from income can be detected by a tax agent, who pays the income to the taxpayer and immediately withholds the tax.

The tax authority can also indicate an overpayment. Then, from the moment the fact of overpayment is discovered (according to paragraph 3 of Article 78, paragraph 4 of Article 79, paragraph 1 of Article 231 of the Tax Code of the Russian Federation), the taxpayer must be notified within 10 working days.

The tax authority notifies of the overpayment in one of the following ways:

- written notice, delivered in person against signature;

- by post with notification;

- indicating the amount of overpayment in the taxpayer’s personal account.

Overpayment refund procedure

Personal income tax is transferred to the budget from the income of an individual. An organization acting as a tax agent does not have the right to pay tax at its own expense. The rules for the return of overpayment of personal income tax were explained in detail by the Arbitration Court of the Moscow District in resolution No. F05-11952/2020 dated August 20, 2020 in case No. A40-263501/2019. The procedure for returning personal income tax depends on the reason for the overpayment:

- The tax agent mistakenly transfers his own funds according to personal income tax details, which were not withheld when paying income to individuals.

- The tax agent made a mistake precisely when withholding personal income tax from the employee’s income - he unlawfully withheld more from him than he should have, or paid out “extra” income from which he withheld personal income tax.

Accordingly, the tax refund procedure will vary.

In the first case, the general rules of Art. 78 of the Tax Code of the Russian Federation, and overpayment of personal income tax is not recognized at all. To return or offset money, an organization should submit an application to the Federal Tax Service at the place of registration. But since the money was transferred using personal income tax details, you will have to additionally confirm that they are not such. To do this, an extract from the tax register for the corresponding tax period must be attached to the application. Also attached to the application is the payment slip on the basis of which the excess amount was deposited.

In the second case, the range of circumstances that need to be documented changes. As the court noted, in this situation, the return of personal income tax to the tax agent is possible only after documents are submitted confirming the settlement of the debt with the individual. And if the corresponding amounts are already included in the 2-NDFL certificates, then you will also need to submit corrective statements.

As a general rule, a tax agent who has excessively withheld personal income tax from an individual’s income is obliged to make a refund independently (clause 14 of article 78, clause 1 of article 231 of the Tax Code of the Russian Federation; clause 34 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2020 No. 57). True, in some cases, you must contact the tax authority for a refund of excessively withheld personal income tax (clause 1.1 of Article 231, Article 231.1 of the Tax Code of the Russian Federation).

To return excessively collected personal income tax from an employee, a special procedure is provided, established by Art. 231 Tax Code of the Russian Federation. The Ministry of Finance drew attention to this in Letter dated July 21, 2020 No. 03-04-06/63250. At the same time, the organization must inform the employee about each fact of overpayment within 10 days.

The employee should submit a written application for the return of the amount of excessively withheld personal income tax in any form. In it you need to indicate the bank account for transferring funds, since the refund of the overpayment is made by the employer only in non-cash form (clause 1 of Article 231 of the Tax Code of the Russian Federation).

There is a deadline for returning an overpayment of personal income tax - it must be returned within three months from the date of receipt of the application (Letter of the Ministry of Finance of the Russian Federation dated July 6, 2021 No. 03-04-10/39533). In case of violation of the tax refund deadline, it will need to be returned with interest, which is accrued for each calendar day of delay based on the key rate of the Central Bank in force on these days (paragraphs three, five, clause 1, article 231 of the Tax Code of the Russian Federation).

Article 231 of the Tax Code of the Russian Federation clearly establishes the sources through which personal income tax can be returned to an employee. These are upcoming payments for personal income tax, withheld and subject to transfer to the budget from income:

• the same employee whose tax was over-withheld;

• other taxpayers for whom the organization acts as a tax agent.

That is, instead of transferring personal income tax to the budget, you need to transfer the amount of over-withheld tax to a specific employee. It does not matter from whose income the tax is withheld: from the salary of the person to whom it is returned, or from the salaries of other employees of the organization.

It may happen that the amount of personal income tax refund to an employee will be more than the three-month amount of calculated and withheld personal income tax for the entire organization. That is, in the next three months there may simply not be enough tax amount to be paid to the budget to refund the tax to the employee. In this case, the tax agent must contact the tax authority at the place of registration with an application for a refund of the overpayment. The application form was approved by Order of the Federal Tax Service dated February 14, 2020 No. ММВ-7-8/ [email protected] You must contact the tax authority within 10 working days from the date of receipt of the application from the employee (paragraphs six, eight, clause 1, article 231 of the Tax Code of the Russian Federation) . In addition to the application, it is necessary to submit (paragraph eight of clause 1 of Article 231 of the Tax Code of the Russian Federation) an extract from the personal income tax register for the corresponding tax period and documents confirming the overpayment.

After receiving an application from an organization, the inspectorate may propose to conduct a joint reconciliation of tax calculations (penalties, fines) (clause 3 of Article 78 of the Tax Code of the Russian Federation). It’s better not to argue and do this, since in this case the Federal Tax Service will offset or return the overpayment to you only after signing the reconciliation report (clauses 3–6 of Article 78 of the Tax Code of the Russian Federation). The tax authority makes a decision on offset or refusal to offset tax amounts within 10 working days from the date of the tax agent’s application (clause 6 of Article 6.1, paragraph two of clause 4 of Article 78 of the Tax Code of the Russian Federation). The inspectorate must inform the tax agent about its decision within five working days after the decision is made (clause 6, article 6.1, clause 9, article 78 of the Tax Code of the Russian Federation). Within a month, the tax authority must transfer money to the organization’s current account (clause 6 of article 78, clause 1 of article 231 of the Tax Code of the Russian Federation). Also, the employer has the right to transfer money to the employee towards the return of personal income tax at his own expense, without waiting for the return of personal income tax from the budget (paragraph nine of paragraph 1 of Article 231 of the Tax Code of the Russian Federation), and then contact the tax office.

If an employee who has been identified as having an excessively withheld amount of tax no longer works for the organization, then he still needs to return the tax (letters from the Ministry of Finance of the Russian Federation dated December 29, 2020 No. 03-04-05/6-1460, dated December 24, 2020 No. 03- 04-05/6-1430). For each individual who has received a refund of tax that was excessively withheld in previous years, submit to the Federal Tax Service a corrective certificate 2-NDFL (section I of the Procedure for filling out a certificate 2-NDFL, letter of the Federal Tax Service dated November 14, 2020 No. BS-4-11 / [email protected] , dated October 26, 2020 No. BS-4-11/ [email protected] ).

How to offset an erroneously transferred personal income tax payment

The taxpayer has the right to timely offset of overpaid amounts of taxes, penalties, and fines (subclause 5, clause 1, article 21 of the Tax Code of the Russian Federation), and the tax authority is obliged to return them (subclause 7, clause 1, article 32 of the Tax Code of the Russian Federation). In general, an erroneously transferred tax amount can be offset against other taxes. From 1 October 2021, this does not require that the type of tax credited be the same.

However, if the tax agent mistakenly transferred excess amounts of tax from his own funds, then the overpaid amount of personal income tax cannot be offset against future personal income tax payments. The tax agent can file a refund claim. Please note: in order to return the overpayment, you must not have arrears on any taxes (penalties, fines). If you have arrears for other federal taxes, penalties or fines, the inspectorate must carry out the offset on its own.

The deadline for submitting an application for credit to the tax authority is three years from the date of payment of the excess tax (Clause 7, Article 78 of the Tax Code of the Russian Federation). Along with the application, you must submit documents that confirm the presence of an overpayment (letters from the Federal Tax Service of the Russian Federation for Moscow dated October 27, 2020 No. 19-19 / [email protected] , Federal Tax Service of the Russian Federation dated February 6, 2017 No. GD-4-8 / [email protected] ).

To return the overpayment for personal income tax, you also need to submit an application for the return of the overpayment to the tax office no later than three years from the date of transfer of the overpaid tax (clause 7 of article 78 of the Tax Code of the Russian Federation). Along with the application, documents confirming the overpaid amount of tax are also submitted: certificates in form 2-NDFL, a register of information on the income of individuals, payment documents confirming the fact of the overpaid tax (paragraph eight of clause 1 of Article 231 of the Tax Code of the Russian Federation).

That is, the tax agent must provide documents from which it will be clear that this overpayment is not tax amounts withheld from the income of individual taxpayers, but is precisely the organization’s funds erroneously transferred to the budget.

In the Letter of the Federal Tax Service of the Russian Federation for Moscow dated October 27, 2020 No. 19-19 / [email protected] attention is drawn to the fact that tax authorities may additionally require data from account 68.1, which reflects personal income tax calculations in accounting for the corresponding period.

There are cases when tax authorities refuse to refund personal income tax, indicating that the overpayment can only be determined based on the results of an on-site tax audit. However, the courts reject the arguments of the tax authorities to confirm the amount of overpayment only by the results of an on-site tax audit if the organization provides evidence of excessive transfer of funds to the budget (Resolution of the Federal Antimonopoly Service of the Moscow Region dated April 30, 2014 No. F05-3657/2014 in case No. A40-91167/13, dated 03/06/2014 No. F05-1184/2014 in case No. A40-80139/13-99-247, AS of the Volga District dated 12/02/2014 No. F06-17741/2013 in case No. A06-166/2014).

Do I need to submit tax registers?

Along with the application, as the tax authorities say, you need to submit an extract from the tax accounting register and the corresponding payment documents that will confirm the presence of an overpayment (letters from the Federal Tax Service of the Russian Federation for Moscow dated October 27, 2020 No. 19-19 / [email protected] , Federal Tax Service of the Russian Federation dated 02/06/2017 No. GD-4-8/ [email protected] ). Confirmation of the correctness of such a requirement of the tax authorities is the Resolution of the Arbitration Court of the Moscow District dated November 24, 2021 No. F05-19418/2020 in case No. A40-335248/2019.

To return the over-transferred personal income tax, the organization-tax agent must submit documents unconditionally confirming the fact of transferring this tax to the budget for a specific individual, and also confirm that in reality the amount of tax in relation to this individual should be less. By virtue of the provisions of Art. 230 of the Tax Code of the Russian Federation, these facts are confirmed precisely by tax accounting registers for personal income tax.

In this regard, as noted by the Arbitration Court of the Moscow District, the Federal Tax Service has the right to refuse a tax refund if the organization, in confirmation of the overpayment, submits only a payment order for the transfer of the total amount of personal income tax without specifying which individual the tax was transferred to. According to the judges, such a document is not evidence of excessive personal income tax payment, since it confirms only the amount paid, but does not provide information about the amount that was withheld during the actual payment of income, nor about the amount that was actually subject to transfer to the relevant individuals. In this case, the presence of an overpayment is revealed precisely by comparing the amounts of tax that must be paid for a certain period with payment documents for this tax relating to the same period.

If the employee returned the excess income

Calculation of personal income tax amounts from income received by an employee is carried out on an accrual basis from the beginning of the calendar year, with the offset of the amount of tax withheld in previous months (clause 3 of Article 226 of the Tax Code of the Russian Federation). In case of payment of a larger salary or vacation pay, tax is paid not at the expense of the tax agent, but at the expense of the income paid to the employee.

The former employee and the organization as a tax agent do not have any additional tax obligations in connection with the write-off of unrefunded debt on wages and vacation pay (for example, upon dismissal). In letters of the Ministry of Finance of the Russian Federation dated July 26, 2018 No. 03-15-06/52554, dated December 26, 2017 No. 03-04-06/86736 and the Federal Tax Service of the Russian Federation for Moscow dated June 28, 2018 No. 20-15/138129, it is noted that the date actual receipt of income in the form of vacation pay is the day of payment. On this day, personal income tax is withheld from vacation pay (Clause 6, Article 226 of the Tax Code of the Russian Federation). Since the amount of tax calculated on vacation pay is withheld on the date of payment, there is no need to re-calculate and withhold personal income tax when the tax agent forgives the employee's debt for unworked vacation days.

If the employee returns the amount of overpaid vacation pay, the amount to be returned is also calculated minus personal income tax. That is, the employee was paid income without personal income tax, and he returns the same amount. The income tax actually becomes paid at the expense of the tax agent and is not a payment of personal income tax (clause 9 of Article 226 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of the Russian Federation dated 02/06/2017 No. GD-4-8 / [email protected] ). The company must adjust vacation pay or wages in the period in which they are accrued and submit an updated calculation for this period. And the overpayment of tax can be returned to the tax agent under Art. 78 of the Tax Code of the Russian Federation, which determines the procedure for offset or refund of amounts of overpaid tax, on the basis of clause 14 of Art. 78 Tax Code of the Russian Federation. In this case, the tax agent has the right to contact the tax authority with an application for the return to the current account of an amount that is not personal income tax and was mistakenly transferred to the budget.

You should pay attention to the situation when an employee quits in January, and he has more vacation debt than accrued payments in the current period. Then, when reimbursing the employer for the debt, a problem arises with reflecting the operation in personal income tax reporting, since the base cannot be adjusted in the current period. There are no negative values when filling out reporting line indicators. Therefore, you should adjust the base for the period of accrual of vacation pay last year. In the current reporting period, the amount of the recalculation made for the previous period is not reflected in the calculation (letter of the Federal Tax Service of the Russian Federation dated August 24, 2017 No. BS-4-11 / [email protected] , dated October 11, 2017 No. GD-4-11/20479). As a rule, personal income tax reports for the previous year have not yet been submitted by the end of January. Therefore, it is necessary to clarify the amount of accruals for the dismissed employee, taking into account the return of the overpayment for leave provided in advance.

Accounting

An amount overpaid to the budget and subsequently returned to the organization does not lead to an increase in the economic benefits of the organization. Consequently, no income is generated in relation to clause 2 of the Accounting Regulations “Income of the Organization” PBU 9/99, approved by Order of the Ministry of Finance of the Russian Federation dated 05/06/1999 No. 32n.

In accounting, the payment of personal income tax (in terms of overpaid funds) is reflected by the entry Debit 68 “Calculations for taxes and fees” Credit 51 “Settlement accounts”. The return by the tax authority of the overpaid amount to the organization's current account is reflected by the reverse entry: Debit 51 Credit 68.

The amount of tax that is excessively withheld from an individual is an error. When it is identified, a primary document is drawn up - an accounting certificate. If the amount is to be returned to the employee, then the error is reflected in the “red reversal” entry: Debit 70 “Settlements with personnel for wages” Credit 68 “Calculations for taxes and fees”.

The transfer of tax to the current account of an individual is reflected by the entry: Debit 70 “Settlements with personnel for wages” and Credit 51 “Current accounts”.

Corporate income tax

The amount of overpaid tax returned from the budget is not taken into account for the purposes of calculating income tax as income, since in this case there is no economic benefit in relation to clause 1 of Art. 41 Tax Code of the Russian Federation.

A similar approach is applied to organizations that apply the simplified tax system (with the object of taxation “Income reduced by the amount of expenses”), and organizations that are taxpayers of the Unified Agricultural Tax (Letter of the Ministry of Finance of the Russian Federation dated June 22, 2009 No. 03-11-11/117, sent by the Letter of the Federal Tax Service RF dated 07/07/2009 No. ШС-17-3/ [email protected] ).

Conditions for crediting amounts of overpaid tax

Article 78 of the current Tax Code of the Russian Federation regulates a certain procedure and conditions, subject to which the offset of amounts of overpaid tax becomes possible and legal.

The main conditions for offset of overpaid amounts are expressed as follows:

- offset can be carried out for certain types of taxes and fees in which a certain amount of overpayment has been identified;

- the offset may apply not only to taxes, but also to penalties, fines and other payments imposed for violation of the established norms of the current tax legislation of the Russian Federation;

- When offsetting the excess transferred amount, fines and penalties cannot be applied to it. Exceptions are cases where acceptable deadlines were violated;

- the established and certified amount may be subject to offset in respect of financial transactions that the taxpayer will only have to make. In this case, the amount of these payments is reduced exactly by the amount of overpaid tax.

It is in the interests of taxpayers to offset the excess amount for previously paid tax. This means that the initial actions and initiative, which is expressed in submitting a written application, must come from them.

Offset of the amount or refund of overpaid taxes, penalties and fines, as a legal procedure, must fully comply with the established norms and conditions.

Otherwise, its result may be annulled by decision of a judicial authority.

Reconciliation of calculations and application for refund of overpaid tax payments

Reconciliation of calculations is a special tax procedure that allows for the most accurate verification and control of all submitted taxpayer data for certain periods.

Before making a decision on offset or refund to the taxpayer of the overpaid amount, a representative of the tax organization is obliged to carry out a lawful joint reconciliation. It can be carried out in relation to: taxes, fees, penalties and fines. The result of the reconciliation is documented in a written act, which is signed by both parties to these legal relations.

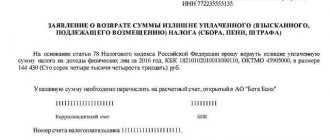

Article 78 establishes that the initial stage of offset or refund of an overpaid amount is the application of the taxpayer and its submission to the tax authority located at the place of registration. The application can also be submitted electronically, but with the obligatory presence of a digital signature. A sample of filling out this document can always be obtained from the nearest tax authority.

The current rules provide that an application for a set-off or refund of an overpaid amount must always contain all necessary accurate information. For example, it must indicate: information about the taxpayer, as well as about the tax authority, information about the exact amount of the overpaid amount, an indication of the specific type of tax or fee, etc.

In addition, the sample document presupposes what exactly the taxpayer wants to receive - a credit for the excess amount, or a full refund.

Rules for the refund of overpaid tax

Article 78 provides that the refund of the amount of overpaid tax is made on the basis of an appropriate decision of the tax authority. A refund is very different from an offset.

If, when offset, the amount is, in fact, simply transferred to pay off other taxes and existing tax debts, then the return means the transfer of this specific amount back to the interested party who submitted the corresponding application - the taxpayer.

At the same time, the current rules and Article 78 provide that a refund can be made only if the taxpayer does not have any arrears or debts.

If there is an arrear, the possibility of returning the overpaid amount remains, but only after additional receipt of financial resources for the initial repayment of the debt.

An application for the return of an overpaid amount can be submitted within 3 years from the date of receipt of this amount in the state current account, or from the date of reconciliation of calculations by the parties.

In cases where the fact of excessive collection of a certain tax has been established and confirmed, the authorized body must decide to return the excess amount of the collected tax, as well as accrued interest, if any.

Review of case No. A48-2866/2018 on the refund of overpaid taxes after three years from the date of payment

The company applied to the court to invalidate the decisions of the Federal Tax Service on the refusal to offset (refund) the amount of tax and the obligation of the tax authority to return the overpaid income tax. The application was satisfied by the decision of the arbitration court of first instance. By the decision of the arbitration court of appeal, the court's decision was left unchanged. The tax authority appealed to the cassation court.

Position of the tax authority:

In accordance with paragraph 1 of Art. 78 of the Tax Code of the Russian Federation, the amount of overpaid tax is subject to offset against the taxpayer’s upcoming payments for this or other taxes, repayment of arrears for other taxes, arrears of penalties and fines for tax offenses, or refund to the taxpayer in the manner prescribed by this article.

According to paragraph 7 of Art. 78 of the Tax Code of the Russian Federation, an application for offset or refund of the amount of overpaid tax can be submitted within three years from the date of payment of the specified amount, unless otherwise provided by the legislation of the Russian Federation on taxes and fees.

The Company should have known about the fact of excessive tax payment from the moment of its actual payment, from which more than three years passed until the filing of an application for the return of the overpayment, in connection with which the Company missed the three-year deadline for filing a claim for the return of the overpayment in court.

Position of the Company:

The Company overpaid income tax due to a decrease in the previously declared amount of income due to the settlement of disagreements with counterparties in court and pre-trial procedures, receipt of compensation for losses, refund of state duty, as well as due to an increase in the previously declared amount of expenses due to non-accounting expenses for services of third parties.

These circumstances became known to the Company after the filing of the initial declaration and payment of the tax amounts calculated therein to the relevant budgets, and the validity of the application to reduce the amount of tax payable was confirmed by the tax authority upon completion of a desk audit of the last updated tax return, as a result of which the decision to involve the Company in responsibility for incomplete payment of tax amounts, or additional tax assessment by the tax authority was not accepted.

Judicial act:

By the decision of the Arbitration Court of the Central District dated February 12, 2019 N F10-6024/2018 in case N A48-2866/2018, the judicial acts of the lower courts were left unchanged, the cassation appeal of the Federal Tax Service was not satisfied.

Arguments of the court:

The Constitutional Court of the Russian Federation, in its Determination of June 21, 2001 N 173-O, formulated a legal position, according to which the period established in Art. 78 of the Tax Code of the Russian Federation, is not aimed at infringing on the rights of a taxpayer who made a mistake in calculating the amount of the tax payment for any reason, including due to ignorance of the tax law or an honest mistake, but, on the contrary, allows him to present to the tax authority, justified and therefore subject to unconditional satisfaction of demands, without resorting to judicial protection of their legitimate interests. At the same time, this provision does not prevent the taxpayer from going to court if the specified deadline is missed.

with a claim for the return of the overpaid amount from the budget in civil or arbitration proceedings.

At the same time, the question of the procedure for calculating the deadline for a taxpayer to submit an application to the court for the return of overpaid tax should be resolved in relation to clause 2 of Art. 79 of the Tax Code of the Russian Federation, taking into account that such an application must be filed within three years from the day when

the person learned or should have learned about the fact of overpaid tax

.

The Supreme Arbitration Court of the Russian Federation in the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation “On some issues arising when arbitration courts apply part one of the Tax Code of the Russian Federation” dated July 30, 2013 N 57, explained that when checking the taxpayer’s compliance with the deadline for filing a claim in court for a refund of overpaid amounts of tax, the courts must take into account that clause 7 of Art.

78 of the Tax Code of the Russian Federation determines the duration and procedure for calculating the period for filing a corresponding application with the tax authority

.

In the event that the tax authority refuses to satisfy the taxpayer’s application for a refund of overpaid amounts of tax, he has the right to go to court with a corresponding claim for tax refund

within the period established by clause 3 of Art.

79 of the Tax Code of the Russian Federation, that is, within three years counting from the day when he learned or should have learned about a violation of his right to a timely offset or refund of tax

.

Similar judicial practice:

Determination of the Constitutional Court of the Russian Federation dated December 21, 2011 N 1665-О-О;

Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 25, 2009 N 12882/08 in case N A65-28187/2007-CA1-56;

Determination of the Constitutional Court of the Russian Federation dated October 1, 2008 N 675-O-P;

Determination of the Constitutional Court of the Russian Federation dated July 3, 2008 N 630-O-P;

Determination of the Supreme Arbitration Court of the Russian Federation dated January 22, 2007 No. 16635/06 in case No. A42-7007/2005.

At the same time, as stated in the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 25, 2009 N 12882/08 in case N A65-28187/2007-CA1-56, the moment when the taxpayer learned about the fact of excessive tax payment cannot be considered the moment he committed actions to adjust your tax liability

and submission of an updated tax return.

The issue of determining the time when the taxpayer learned or should have learned about the excessive payment of tax should be resolved taking into account the assessment of the totality of all circumstances relevant to the case, in particular, to establish the reason why the taxpayer overpaid the tax; whether he has the opportunity to correctly calculate tax according to the initial tax return, changes in current legislation during the tax period in question, as well as other circumstances that may be recognized by the court as sufficient to recognize the deadline for tax refund as not being missed.

The burden of proving these circumstances, by virtue of Article 65 of the Arbitration Procedural Code of the Russian Federation, rests on the taxpayer.

Deadline for refund of overpaid tax

The provisions of tax legislation and Article 78 of the Tax Code of the Russian Federation establish acceptable periods within which amounts overpaid to the state budget must be returned to taxpayers.

The excess amount of previously paid tax must be fully refunded to the applicant within one calendar month.

The reference date must be considered the day of filing a written application for return to the relevant authority.

In addition, Article 78 provides that if the tax authority has legitimate grounds for refusing to refund an overpaid amount, they must be presented to the taxpayer also within one month from the date of submission of a written application.

If the taxpayer does not agree with the decision of the tax authority, he always has the right to go to court in order to protect his own interests. In this case, the claim will need to be accompanied by relevant evidence that will confirm that the refusal issued by the tax authority cannot be considered justified and lawful.

An interested person can apply to a judicial authority even if, within one month from the date of the taxpayer’s application, the tax inspectorate has not submitted its official response to his application, and also has not provided a refund.

Author of the article

What to do if you missed the three-year deadline

As a general rule, the period for offset or refund of overpayment is three years from the date of payment of the tax. If three years have passed, the tax office will refuse.

However, the three-year period is not always counted from the date of payment. For example, an overpayment arose due to the payment of advance payments for income tax. And the accountant found out about it when he filed a declaration at the end of the year.

Therefore, if the tax office refused you, check whether you knew about the overpayment at the moment it arose. Or, for objective reasons, you found out about it later.

If three years have not yet elapsed from the day the taxpayer actually learned about the surplus, you can go to court. The court considers the period to be three years from the moment the company learned or should have known about the overpayment. In this case, the judge will check the reasons why the company or individual entrepreneur could not find out about the overpayment earlier.

For example

, filed an income tax return and paid tax for 2016 on March 13, 2021. On March 20, 2021, the company filed an updated declaration for 2021. In it, it added expenses that it could not reflect in the initial declaration due to a legal dispute with the counterparty. As a result, after submitting the updated declaration, an overpayment arose. On July 10, 2021, the company filed an application for a refund of overpaid taxes. The inspectorate refused to refund the tax because more than three years had passed since its payment (March 13, 2021). However, the organization can obtain a tax refund through the court, since it became aware of the overpayment only on March 20, 2021, when the accounting data was adjusted. If we count three years from this date, then at the time of filing the application the return period has not yet passed.